A Handbook Of (Mostly Failed) Radical Inflation-Fighting Efforts

More governments are seeking ways to prevent surging inflation whipping up economic trouble – and even public unrest – without raising interest rates.

But as the examples below show, past attempts to rein in soaring prices without hiking borrowing costs have often ended badly.

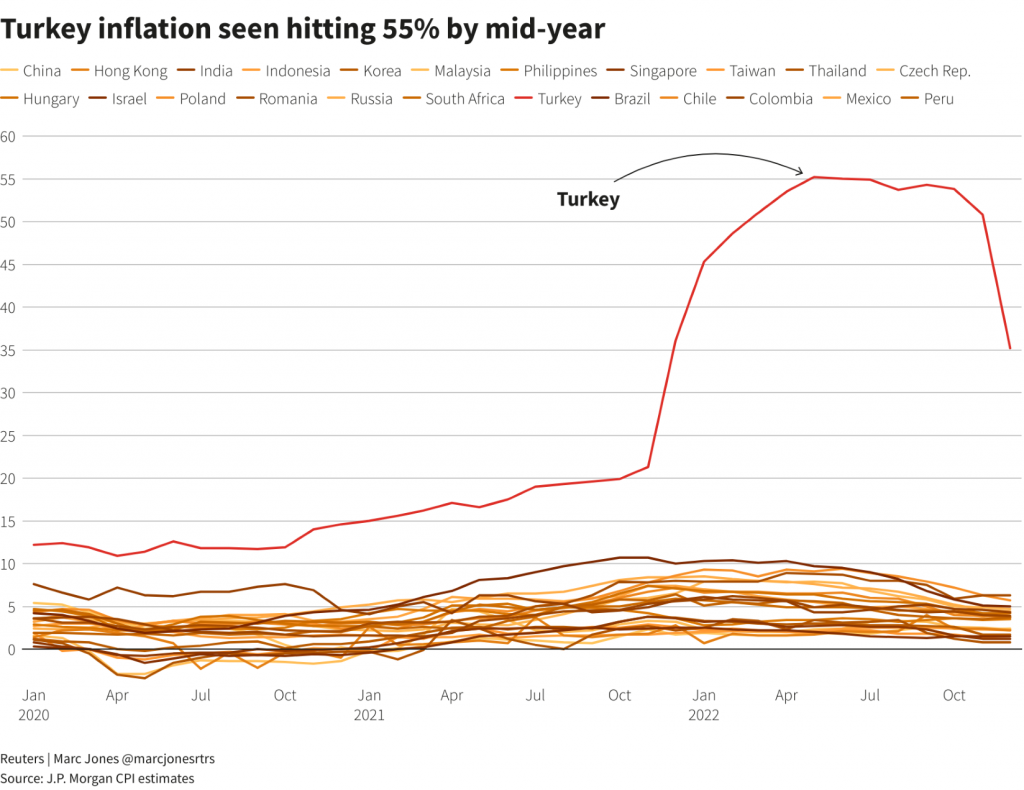

TURKEY

Turkey has spent years slashing rates only to hike again when the lira collapses, stoking inflation.

It has dabbled with measures including FX restrictions, but this time President Tayyip Erdogan is going all-in by offering to compensate lira savers from the public purse if currency losses exceed bank account interest rates.

That could prove costly, and put at risk a main draw for foreign investors – Turkey’s relatively low government debt.

“What the Turks are trying, honestly – I have never seen anything like it before,” said AXA’s chief economist Gilles Moec.

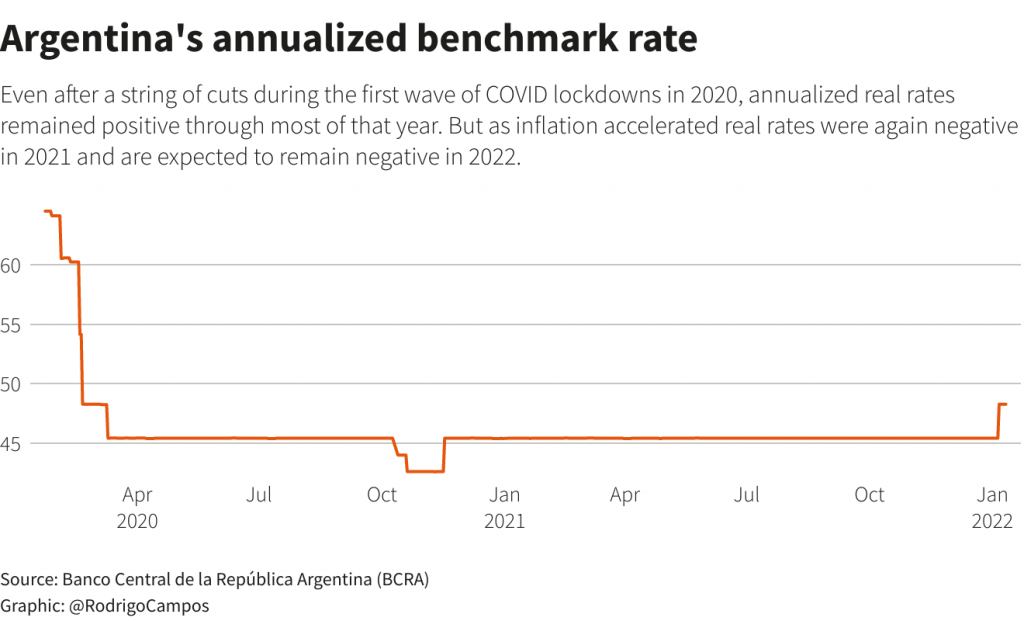

ARGENTINA

A lack of trust in economic institutions – and the peso – has plagued Argentina for decades.

Efforts by right- and left-wing governments to rein in galloping inflation have seen price freezes on many products and capital controls.

Argentines often prefer to do business in dollars but limited access to the U.S. currency has created a huge gap between official and black market exchange rates.

The central bank recently raised interest rates to 40% from 38%. But the “real” rate, taking inflation into account, remains deeply negative.

Goldman Sachs’ Argentina economist Alberto Ramos says headline inflation has averaged 47.2% since July 2018, attesting to “significant macro policy dysfunction and the failure of the monetary authority in securing monetary control”.

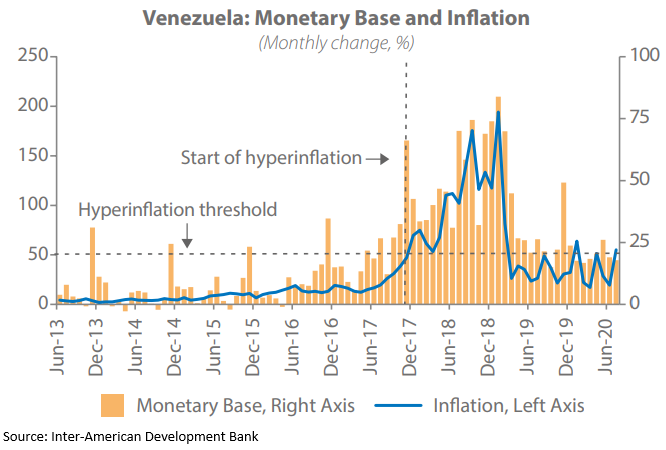

VENEZUELA

Hard-left governments have tried virtually everything over two decades, from fixing prices in 2007 to offering cut-price dollars – a policy quickly reversed due to frenzied demand.

Venezuela defaulted in 2017 and money-printing to cover the budget deficit caused hyperinflation which reached 65,000% in 2018. The IMF sees inflation at 2,000% this year.

President Nicholas Maduro eased some price controls in 2019 and lifted a ban on foreign currency transactions. Official and unofficial exchange rates were brought into line but the bolivar plunged 8,000% and Venezuela’s debt-to-GDP ratio soared to 500%.

Last month Reuters reported the government was paying providers in dollars to help control inflation.

But the Inter-American Development Bank and others have warned that such ‘dollarisation’ leaves those unable to obtain dollars with little access to basic goods, including food.

BRAZIL

High inflation in the 1980s became hyperinflation in the 1990s, just as Brazil returned to democracy.

Under then-president Fernando Collor de Mello, prices, wages and 80% of private assets were frozen and financial transactions heavily taxed.

Inflation peaked near 3,000% in 1990 and though it dropped to 433% in 1991 it was back to almost 2,000% by 1993.

The ‘Real Plan’ of 1994 brought things under control, establishing a new currency, hiking rates and slashing spending. Since 1997, inflation has been in single digits every year but one.

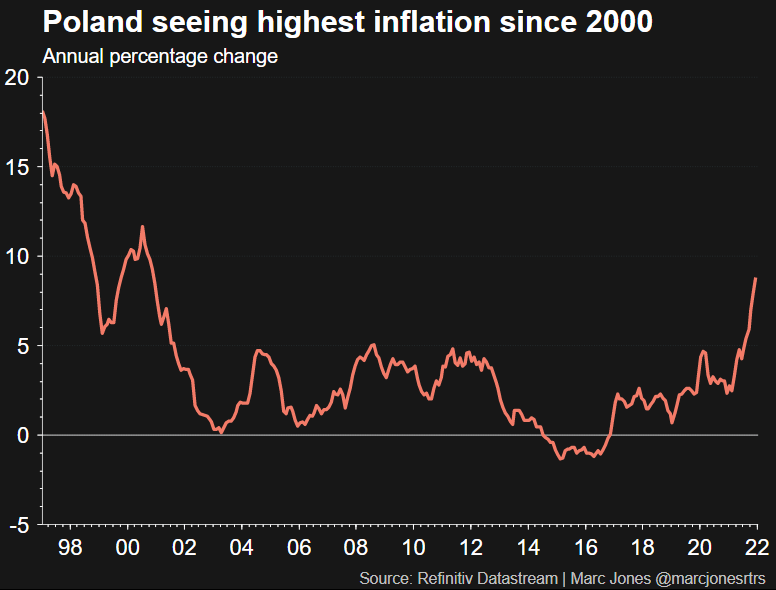

POLAND

Poland’s “anti-inflation shield 2.0” includes temporary cuts in value-added tax (VAT) on fuel, food and fertilisers to offset annual price growth that could hit double digits for the first time since 2000.

JPMorgan reckons last week’s measures and November’s Shield 1.0 will reduce inflation by 3 percentage points by mid-year, while Poland’s prime minister estimates Shields 1.0 and 2.0 will cost up to 30 billion zloty ($7.53 billion) — nearly 1% of GDP.

But “maintaining an optically lower CPI is a lost battle if price pressures prove persistent”, said JPMorgan’s José Cerveira.

CONGO AND ZIMBABWE

Prices in Democratic Republic of Congo rose by a cumulative 6.3 billion percent in first half of the 1990s as budget deficits were financed with rampant money-printing.

Monetary and fiscal policy restraint and a floating exchange rate system brought hyperinflation under control in 2001.

Zimbabwe printed so much money — including a Z$100 trillion banknote — that its inflation rate hit 500 billion percent in 2008, rendering the currency almost worthless.

Price ceilings imposed by the government left sellers unable to make a profit, leading to major shortages.

By late 2008 Zimbabweans were using U.S. dollars for transactions and in 2009 a multicurrency system also including South Africa’s rand was introduced.

A new Zimbabwe dollar was launched in 2019 but Harare was forced to return to the multicurrency set-up when COVID-19 struck in 2020, pushing inflation to an IMF-reported 349%.

FRANCE

Hyperinflation during the French Revolution saw monthly price rises peak at 143%. The 1793 “Law of the General Maximum” responded with price limits and the death penalty for price ‘gouging’.

Historians say it was mostly a failure, as traders forced to sell at below cost price turned to the black market or kept goods for themselves, resulting in major shortages.

MEXICO

Falling oil prices and U.S. rate hikes halted Mexico’s economic boom in 1980-81 and left the peso’s dollar peg under strain, with capital flight and dwindling FX reserves forcing a 260% devaluation in 1982.

Dollar bank deposits were converted into pesos and a moratorium declared on debt payments. By year-end, all trade became regulated, full capital controls were adopted and banks were nationalised.

Annual inflation neared 100% in 1982-83 as real per capita GDP slumped. It stayed high, topping 150% in 1987.

In 1994 the peso crisis — which spread to other emerging economies — forced a free float that saw the currency dive in value. Mexico’s banking sector collapsed and the country needed a $50 billion international bailout to avoid default.

A severe recession and more hyperinflation followed but by 2002 Mexico held investment-grade credit ratings.

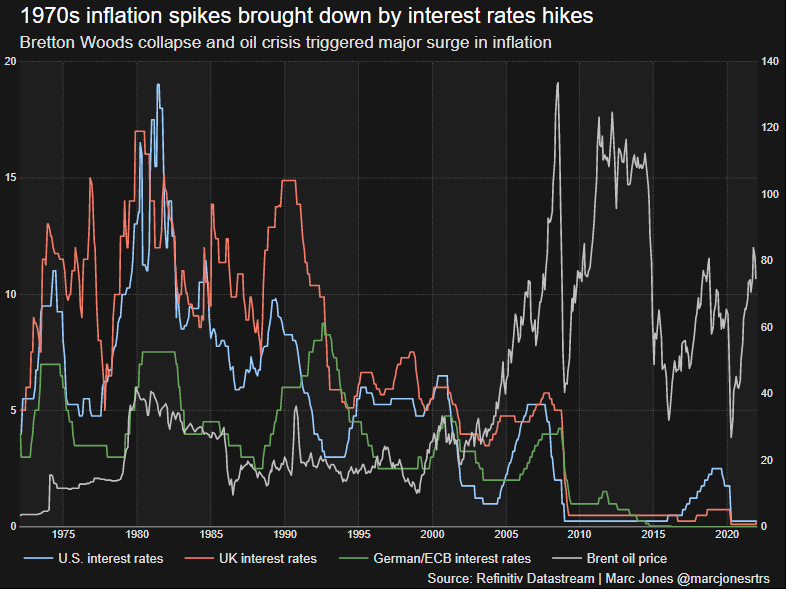

THE 1970s

Many countries turned to price controls after the Bretton Woods system of fixed exchange rates collapsed in 1971 and the 1973 oil crisis triggered a worldwide surge in inflation.

After withdrawing from Bretton Woods, the United States imposed a 90-day freeze on prices and wages for the first time since World War Two.

It was considered a political success but turned into economic failure, ushering in stagflation and currency instability. The dollar plunged by a third during the 1970s.

France also brought in price controls, as did Britain where inflation neared 25%. The unpopular policy helped trigger labour strikes that marked the 1978-79 “Winter of Discontent”.

Inflation receded in the early 1980s after interest rate hikes and an easing in oil prices.

“History tells you it never works,” AXA’s Moec said of price and wage caps. “But it doesn’t stop people from trying.”

(Reporting by Marc Jones in London and Rodrigo Campos in New York; Editing by Catherine Evans)

Trending across pm today

- How To Adapt To A Flat Hierarchy In Your Business

David Amor

- Spotify Scaling Agile Model

Abhishek Mishra

- Conjugate Italian Verbs: A Comprehensive Guide For Mastery

PM Today Contri...

- How To Use And Buy An Oyster Card In London

News Team

- Increasing The Scope Of Customer Service Through Simple Internal Practices

PM Today Contri...